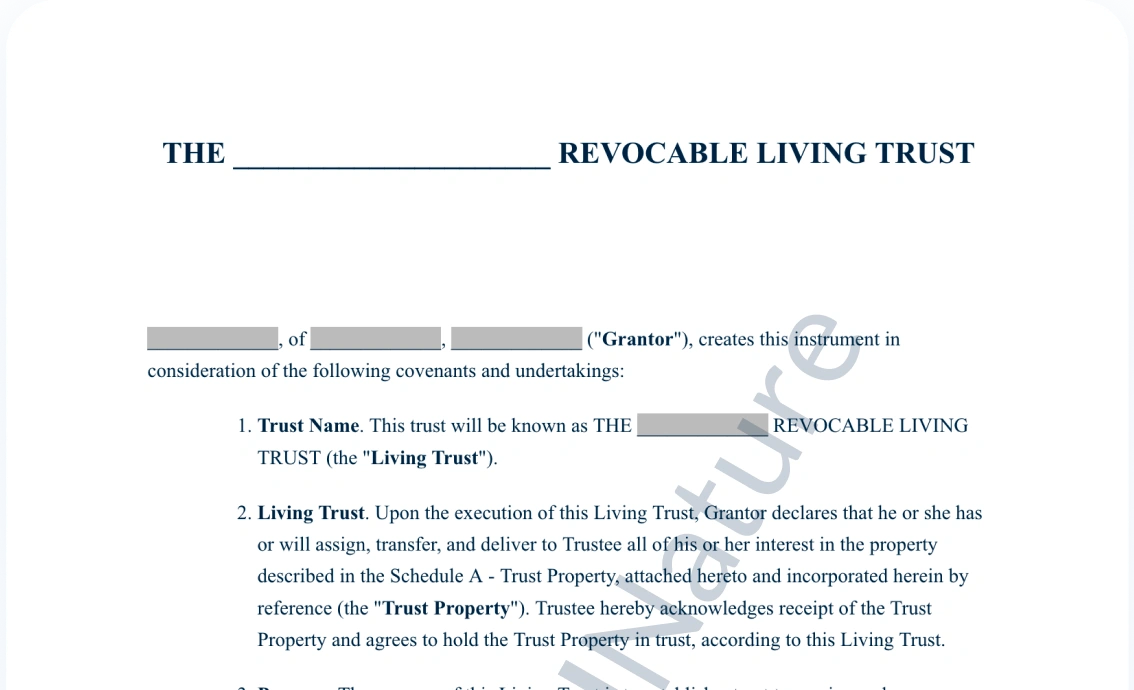

Revocable Living Trust

A revocable living trust is an essential estate planning tool used for securing one's assets during life and then efficiently transferring those assets upon death.

Select a state

What is a revocable living trust?

A revocable living trust is a legal arrangement that allows an individual (the “grantor,” “settlor,” or “trustor”) to transfer ownership of their assets into a trust during their lifetime, with the flexibility to change or revoke the trust at any time while they are alive. Trusts are evidenced by a legal document often called a "trust instrument."

Choose the best estate planning document for you

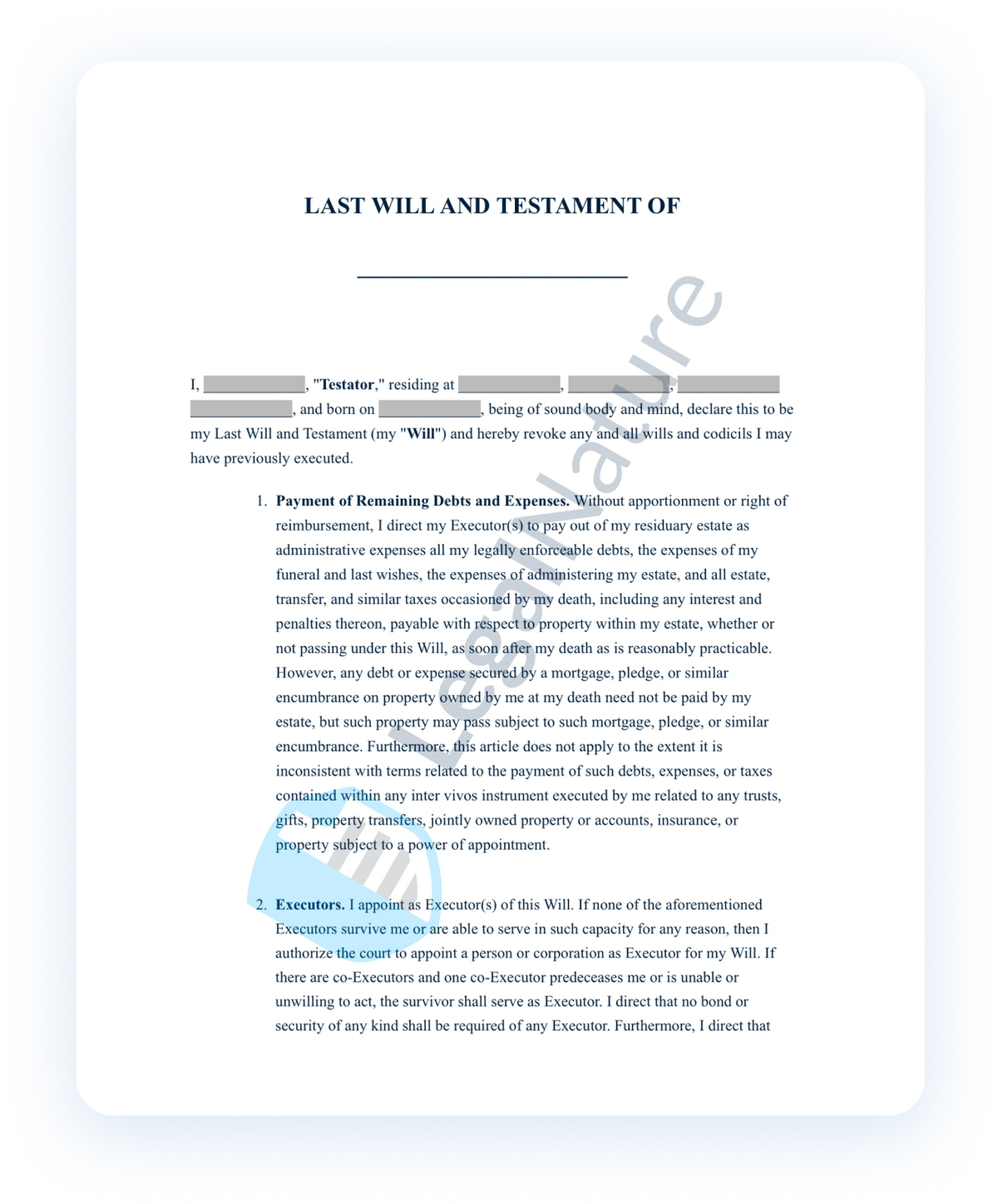

Last Will and Testament This legal document outlines how you want your assets and property to be distributed after death.

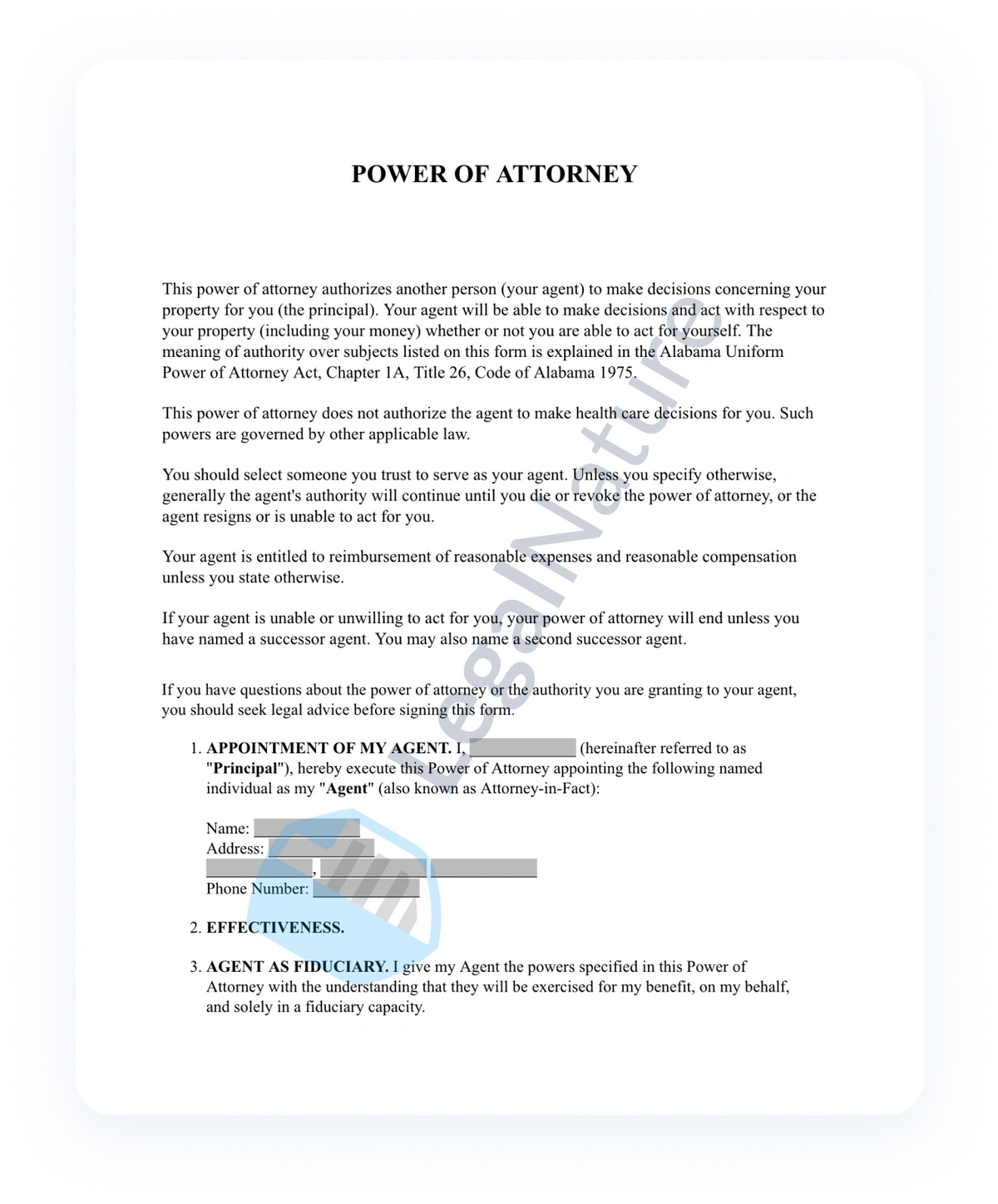

Power of Attorney Grant an attorney-in-fact, or agent, the legal authority to make legal and financial decisions on your behalf.

Create a revocable living trust in your state

When to use a revocable living trust

A revocable living trust is a useful estate planning tool that is most beneficial for use in the following situations:

- Avoiding Probate: If you want your assets to bypass the probate process, which can be lengthy, costly, and public, then a revocable living trust is an effective tool. Assets held in the trust transfer directly to beneficiaries without court involvement, streamlining the distribution and maintaining privacy.

- Owning Property in Multiple States: If you own real estate in more than one state, a revocable living trust helps you avoid “ancillary probate” in each state, saving time and reducing legal complexity for your heirs.

- Desiring Privacy: Probate proceedings are public, but assets in a revocable living trust are distributed privately, keeping your estate details out of the public record.

- Complex or Large Estates: For individuals with complex estates, business interests, or specific instructions for asset distribution, a revocable living trust offers flexibility and control, allowing you to set conditions for distributions and manage assets efficiently.

- Continuity of Asset Management: Trusts can provide uninterrupted management of investments and other assets if you become unable to manage them yourself, unlike a will, which only takes effect after death.

Create your revocable living trust in 3 easy steps

Gather Information

Begin by adding the relevant information for each Grantor, such as name and address. Grantors are the people creating, funding, and signing the revocable living trust's documentation.

Describe the Assets

Enter the name, description, and value of each asset that will be added to the trust. It is very important to provide a description that specifically identifies the asset in order to avoid unwanted confusion.

Review

After completing your revocable living trust, be sure to review it thoroughly to ensure that it meets your needs. You may make textual edits if you wish. If no changes are needed, you can sign the document and have it notarized.

Why create a revocable living trust?

Revocable living trusts are created in order to avoid or reduce the costs of probate, maintain privacy of an estate, retain control and flexibility over the management of estate assets, and to streamline the transfer of assets to beneficiaries. Revocable living trusts may be tailored to your specific situation and estate needs, including conditions and instructions for asset distribution. Revocable living trusts may also be changed or revoked at any time while you are alive and competent.

Why choose LegalNature?

Revocable Living Trust Guide

This guide contains a description of the main sections of our revocable living trust. Note that some of the sections are optional depending on how you answer our questionnaire.

Introductory Language

The first section identifies the grantor. If applicable, it will also state that the grantor will act as the initial trustee.

Trust Name

This section identifies the official name of the trust. Use this name when referring to the trust in other documents and when transferring assets to the trust.

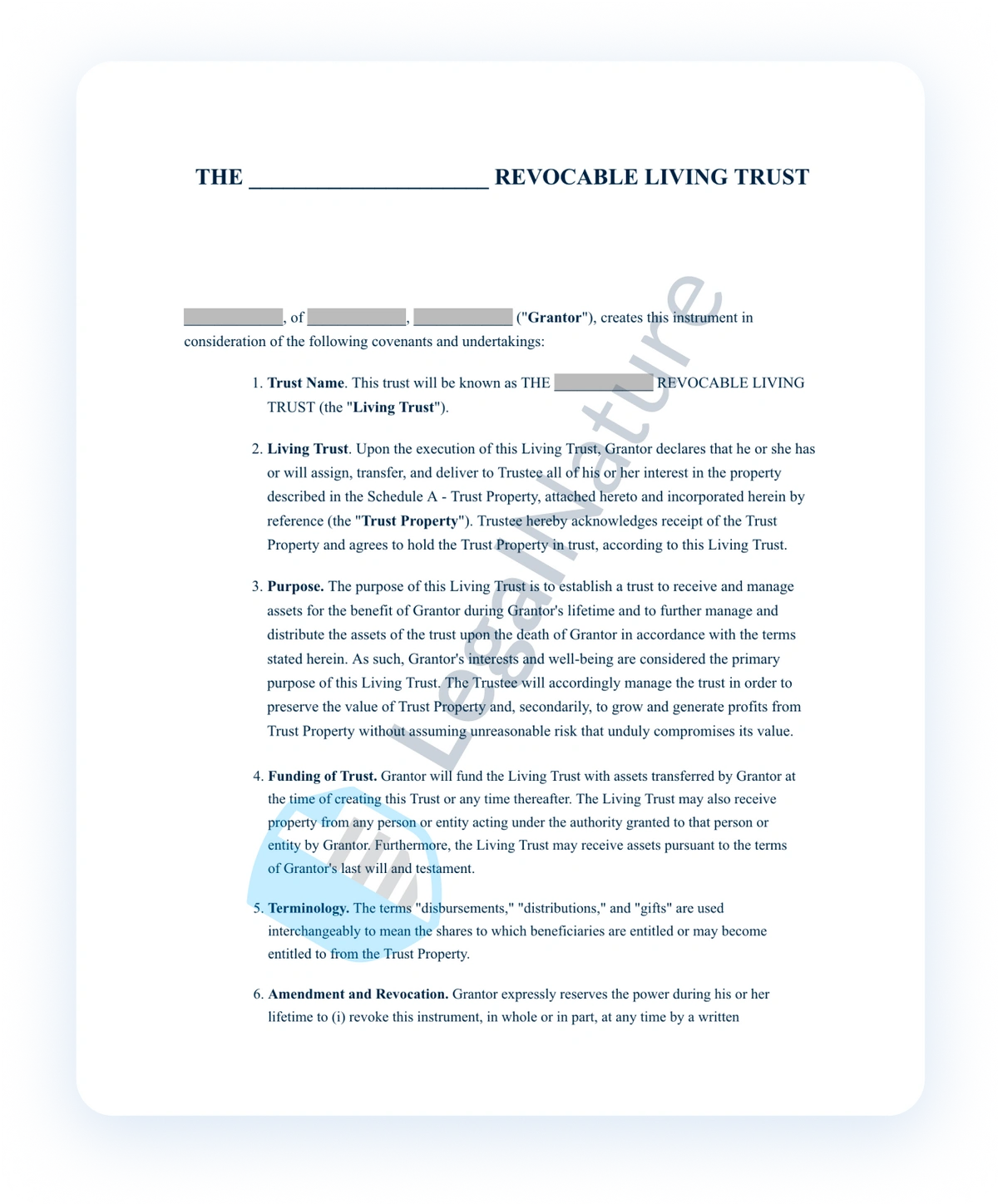

Purpose

The next section explains that the general trust's purpose is to receive and manage assets during the grantor’s lifetime and to distribute those assets according to the grantor’s wishes upon death. Carrying out the grantor’s wishes is the primary purpose of the trust, and any successor trustee must act accordingly when managing the trust.

Funding the Trust

The grantor will fund the trust by transferring specific assets to the trust, such as personal or real property, at the time of creating it or any time thereafter. The grantor may also remove trust assets at any time while living.

Amendment and Revocation

The grantor can change or terminate the trust at any time during his or her lifetime.

Withdrawal by Grantor

The grantor may make additions or withdrawals from the trust at any time.

Death of Grantor

When the grantor dies, the trust becomes irrevocable. This means that at that time, it may not be amended or altered.

Trustees

This section identifies the initial trustees and any successor trustees appointed by the grantor to manage the trust. A trustee may resign by providing 30 days' notice to the next successor trustee.

The grantor may remove an appointed trustee at any time during the grantor’s lifetime by notifying that trustee, and the grantor may appoint additional or replacement trustees at any time.

Bond

This section explains whether or not the trustees are required to post a bond. A bond is insurance to protect the trust in the event that the trustee acts dishonestly or imprudently with trust property. Payment for the bond is usually a small fee relative to the size of the trust and comes out of the trust property.

If the grantor only wants specific appointed trustees to serve with a bond, then you can manually add this language by downloading and changing the Word document version of your completed trust from our site.

Compensation

If an appointed trustee is an individual, then he or she is not entitled to compensation for acting as the trustee under the terms of this section. However, if a trustee is a professional trustee service or business entity, then the trustee will be entitled to the customary and reasonable compensation in rendering such services.

Liability of Trustee

The trustee will not be liable for any improper actions taken so long as those actions are taken in good faith when carrying out his or her duties.

Trustee's Management Powers and Duties

When transacting business on behalf of the trust, the trustee may use the following format when identifying the trust: "John Doe, as Trustee of The [Grantor’s name] Revocable Living Trust, dated [month] [day], [year]. The trustee has all the rights and powers available under state law to carry out the grantor’s wishes." Note, however, that the trustee may ONLY use such powers if they help carry out the grantor’s wishes.

Accounting

After the grantor’s death, the trustee is required to provide semi-annual accounting to adult beneficiaries detailing relevant transactions and dealings of the trust funds.

Spouse's Subtrust

If you choose the option to include trust funds specifically for the grantor’s spouse, then this section is included and details the terms of the spousal trust fund. The property set aside for the spouse is identified on the schedule titled “Spousal Subtrust Property” attached at the end of the document.

After the grantor’s death, the trustee will maintain such funds and make periodic disbursements to the spouse as the trustee considers appropriate for the spouse's care, protection, health, education, maintenance, and support, taking into account the spouse’s accustomed manner of living.

If the spouse does not survive the grantor, then the funds set aside for the spouse will be put into the general trust fund and go to the general trust beneficiaries that the grantor designated.

Note that before the grantor’s death, the grantor may still use the trust funds for spousal support since the grantor still has control over the trust.

Children's Subtrust

If you choose the option to include trust funds specifically for the grantor’s children, then this section details the terms of such trust funds. First, this section identifies the children that are eligible to receive trust funds. If you choose the relevant option, any after-born or after-adopted children are also included. The property set aside for the children is identified on the schedule titled “Child Subtrust Property” attached at the end of the document.

After the grantor’s death, the trustee will maintain the funds and make periodic disbursements to the children as the trustee considers appropriate for their care, protection, health, education, maintenance, and support, taking into account their accustomed manner of living.

If you select the relevant option, then this section also specifies the age that each child will stop receiving payments. In this case, the child will receive the rest of his or her equal share upon reaching the specified age. If you do not select this option, then the children will continue to receive payments until the trust fund is completely diminished.

If a child dies before receiving his or her full share, then that child’s share will go to his or her living descendants; if no descendants exist, then the share will go to the grantor’s living descendants.

Note that before the grantor’s death, the grantor may still use trust funds for supporting the children since the grantor still has control over the trust.

Payment to Minors

As to any minor beneficiaries under the trust—including the grantor’s children, if any—the trustee has discretion as to whether or not to make payments directly to the minor, to make payments to the minor’s legal guardian or caretaker, or to withhold payments and invest the funds until the child is no longer a minor.

Pet Care

If you choose to include this option, this section identifies a caregiver to receive and care for the grantor’s pets upon the grantor’s death. It also names an alternative caregiver in case the first is unable to serve. You also have the option to provide trust funds for the caregiver to use in supporting the pets. Lastly, this section identifies the pets involved and provides any other instructions you choose to include.

Other Gifts and Beneficiaries

This section lists any specific gifts from the trust property that the grantor wants distributed upon his or her death. Each gift names a beneficiary to receive it. If you name co-beneficiaries, then they will divide the property equally. Also, this section names alternative beneficiaries to receive the gift in case the first-choice beneficiaries do not outlive the grantor. These assets are also listed under the general trust property.

Remaining Trust Property

This important section names the beneficiary that will receive any remaining trust property after any and all specific gifts, spousal trust funds, and child trust funds are accounted for. Think of this as a catch-all clause that tells the trustee what to do with any leftover property. Typically, this property is left to the grantor’s spouse and then any children as alternative co-beneficiaries. Other common beneficiaries are close family and friends or favorite charities.

Intentional Omissions

If you choose to include this option, then this section identifies any specific persons who are intentionally not named as beneficiaries to receive anything under the trust. It is important to list any people that may try to make a claim against the grantor’s property to whom the grantor specifically does not want to give anything. Common candidates are estranged family members and ex-spouses.

Government Benefits

The trustee is prohibited from making a disbursement that will disqualify a beneficiary from eligibility for government benefits and entitlement programs unless it is in the best interests of the beneficiary to do so. Still, the trustee cannot be held responsible if a beneficiary fails to maintain eligibility due to receiving a disbursement under the trust.

Incapacity of Grantor

If the grantor is also the initial trustee and the grantor becomes incapacitated, then the next successor trustee will become trustee. Here, the term "incapacitated" means the inability to make informed decisions because of advanced age, illness, or other causes.

The grantor’s healthcare agent under a healthcare power of attorney will make the decision as to whether the grantor is incapacitated, along with a concurring opinion of at least one physician. If no healthcare agent is available, then the successor trustee you name in this section will have the authority to make this decision.

Terms of Property Distribution

A beneficiary is required to survive the grantor by at least 30 days in order to receive property under the trust. If there is no surviving beneficiary to receive a gift, then that gift will go to the beneficiary’s lineal descendants.

Priority of Distributions

If the value of the remaining trust property is insufficient to fund a gift, then the trustee will have absolute authority to determine which of the remaining gifts listed under the trust will be distributed. However, remember that the trustee must always seek to carry out the grantor’s wishes; therefore, the trustee will take any known preferences of the grantor into account when making this determination.

Liquidation of Trust

If the value of the trust property becomes diminished to the point that only insignificant sums of money remain, then the trustee has the power to distribute all the remaining funds. This helps avoid any ongoing fees against the trust property.

Merging of Similar Trusts

This language helps to avoid duplicate fees against the trust that may occur in the event that two separate trust funds end up benefiting the same beneficiary. In such a scenario, the trustee is authorized to merge the separate funds together to make things simpler.

Powers Concerning Insurance Policies

The grantor reserves the right to sell, assign, or gift any insurance policies held under the trust in any manner the grantor wishes. The trustee will use his or her best efforts to collect any sums due under an insurance policy, but will not be required to institute legal proceedings to collect such sums unless the trustee is indemnified against liability.

Spendthrift Provision

This provision prevents creditors from making a claim against a gift before that gift is actually distributed to its beneficiary.

Gifts Given to a Beneficiary during Grantor's Lifetime

A gift that is given to a beneficiary during the grantor’s lifetime that is the same as a gift going to the beneficiary under the trust will satisfy the terms of the trust, and, therefore, that beneficiary will not receive the same gift twice.

Grantor's Right to Homestead Tax Exemption

If the grantor’s main residence is held in the trust, then the grantor has the right to still occupy and use the residence rent free during their lifetime. This right helps to ensure that the grantor will not lose eligibility for any state homestead tax exemptions that he or she may qualify for.

Fiduciary Conflicts of Interest

A trustee with a conflict of interest may still transact business with the trust and continue serving as trustee so long as the trustee acts in good faith, with reasonable care, and on terms comparable to those that may be obtained from third parties when transacting business related to the trust.

Notice of Events

The trustee will not be responsible for good faith errors made when making distributions to beneficiaries who no longer have the right to receive such distributions due to a change in circumstances for which the trustee does not receive notice; for example, a death, birth, marriage, or similar event. However, the trustee will still have to try to recover any such improper distributions.

Change of Situs

The trustee may choose to move the trust to a new jurisdiction at any time. For instance, the trustee may move the trust to a different state, and that state’s laws will then govern the trust. This power may be exercised multiple times and will be final and binding on all individuals and entities involved.

Liability for Acts of Predecessors

Trustees may not be held responsible for any improper actions taken by a prior trustee.

Certificate of Trust

A trustee may sign a certificate or abstract of trust before a notary public containing information describing aspects of this trust, and the certificate or abstract will serve as conclusive evidence of the facts it contains. Third parties transacting with the trust may therefore rely on such certificates or abstracts as accurate representations of trust information.

Governing Law

This section identifies the state law currently governing the trust.

Certification of Grantor

Here, the grantor signs and dates where indicated to confirm that he or she has read the trust and approved of its terms.

Notary Acknowledgment

Using a notary to witness the signing is optional but recommended, as it provides additional evidence of the authenticity of the trust should it ever be disputed.

Frequently asked questions

What is required to make a revocable living trust legal?

Trust law is state specific, so the formalities to create a valid revocable living trust may vary from state to state.

In every jurisdiction, the person creating the trust (the “grantor”) must be at least 18 years old and must have the mental capacity to understand his or her actions at the time the trust agreement is signed.

Some states require that the grantor’s signature be witnessed and/or notarized when the document is signed.

If I have a trust, do I still need a will?

Yes, you still need a last will and testament. If you create a joint revocable living trust, then each grantor still needs a separate will. Even though a revocable living trust is an important estate planning document, it does not replace a will.

Firstly, a living trust will never include all the property you own. In the event of your death, you will need a way to transfer any assets not placed into the living trust to your desired beneficiaries. This is accomplished by using a special type of will called a pour-over will. Secondly, if you have children or other dependents, a living trust does not enable you to name guardians. Lastly, in a will you also have the opportunity to express your burial wishes.

Who can be a beneficiary of a revocable living trust?

Any natural person and any organization can be named as a trust beneficiary.

In the case of a beneficiary who is a minor, the trust can include provisions designed to govern distributions and provide some structure and control over the assets until the minor beneficiary reaches a pre-determined age (or ages).

In most states, it is not legal to name a pet as a beneficiary in a revocable living trust.

I am married. Should I establish a joint revocable living trust with my spouse, or should we each have our own individual revocable living trusts?

Unlike a last will and testament, which is specific to individual people, you can create either separate revocable living trusts or a joint revocable living trust with someone else.

If most of the assets that you will be using to fund the trust are owned jointly with another person and if your distribution wishes are the same, then regardless of who dies first, using a joint revocable living trust may make the most sense. With a joint revocable living trust, both parties normally serve as grantors and as co-trustees.

What does it mean to “fund” a revocable living trust?

Establishing a revocable living trust is just the first step in creating your trust. In order to make your new trust legal, you will need to put assets into it. This process is referred to as “funding” the trust.

You can put a wide variety of assets into a trust. The following assets are some of the most commonly used to fund a trust:

- Real estate – You can transfer real estate to a trust through a quit claim deed, warranty deed, or transfer on death deed (if available in your state).

- Bank accounts – Your checking and savings accounts can be retitled into the name of your new trust.

- Stocks and bonds – By contacting the transfer agent or your investment professional, you may be able to retitle your non-retirement investments so that your trust is the nominal owner.

- Tangible personal property – You can retitle motor vehicles, boats, and other items of tangible personal property so that the trust owns them.

- Beneficiary changes – You can also make the trust the beneficiary of your retirement accounts and life insurance, so that assets pass according to the terms defined in the trust agreement.

Other assets that can be placed into or directed toward a revocable living trust include contracts for deeds or mortgages where someone else is paying you. An “assignment of interest” can also be used to transfer household goods and other assets into your new trust.

Create your revocable living trust in minutes

Complete our form

;fill-opacity:1;'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M7.17816%205.46484C8.48591%205.46484%209.81742%206.23165%2011.1727%207.76529C10.8517%208.08628%2010.6467%208.28838%2010.5575%208.3716C10.4683%208.45482%2010.2514%208.6391%209.90659%208.92442C9.56182%209.20975%209.28244%209.40591%209.06844%209.51291C8.85445%209.6199%208.5721%209.73285%208.22138%209.85173C7.87067%209.97062%207.52293%2010.0301%207.17816%2010.0301C6.75017%2010.0301%206.35785%209.97656%206.00119%209.86957C5.64453%209.76257%205.28788%209.5783%204.93122%209.31675C4.57456%209.0552%204.29518%208.83229%204.09307%208.64801C3.89096%208.46374%203.58781%208.16355%203.18359%207.74745C3.95636%206.97469%204.64291%206.40107%205.24329%206.02658C5.84367%205.65209%206.48862%205.46484%207.17816%205.46484ZM7.17816%209.37024C7.61804%209.37024%207.9955%209.20975%208.31055%208.88876C8.6256%208.56776%208.78312%208.18733%208.78312%207.74745C8.78312%207.30757%208.6256%206.92714%208.31055%206.60615C7.9955%206.28516%207.61804%206.12466%207.17816%206.12466C6.73828%206.12466%206.36082%206.28516%206.04577%206.60615C5.73072%206.92714%205.5732%207.30757%205.5732%207.74745C5.5732%208.18733%205.73072%208.56776%206.04577%208.88876C6.36082%209.20975%206.73828%209.37024%207.17816%209.37024ZM7.17816%207.1768C7.17816%207.34324%207.23166%207.47996%207.33865%207.58696C7.44565%207.69395%207.58237%207.74745%207.74881%207.74745C7.8677%207.74745%207.98658%207.70584%208.10547%207.62262V7.74745C8.10547%208.009%208.01631%208.23191%207.83798%208.41619C7.65965%208.60046%207.43971%208.6926%207.17816%208.6926C6.91661%208.6926%206.69667%208.60046%206.51834%208.41619C6.34001%208.23191%206.25085%208.009%206.25085%207.74745C6.25085%207.4859%206.34001%207.26299%206.51834%207.07872C6.69667%206.89444%206.91661%206.80231%207.17816%206.80231H7.32082C7.22571%206.9212%207.17816%207.04603%207.17816%207.1768Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/svg%3e)

Preview and download your document

;fill-opacity:1;'/%3e%3cg%20clip-path='url(%23clip0_10486_8655)'%3e%3cpath%20d='M10.8931%205.49519C10.8004%205.45343%2010.6879%205.48908%2010.6427%205.57565L10.4595%205.92398L10.3128%205.85879L10.5058%205.49212L10.5069%205.48906C10.508%205.48703%2010.5091%205.48397%2010.5103%205.48194C10.54%205.4137%2010.5743%205.33324%2010.5864%205.24258C10.6239%204.97267%2010.5125%204.68749%2010.2874%204.47869C10.0733%204.28007%209.74562%204.16804%209.43445%204.18534C9.36934%204.18942%209.29984%204.20062%209.22812%204.21998C9.11446%204.25053%209.00302%204.30349%208.8982%204.37785C8.82316%204.4308%208.71833%204.52146%208.64661%204.64877L8.64551%204.65184L8.64441%204.65387L7.9603%205.95657C7.95698%205.96166%207.95369%205.96675%207.95037%205.97286C7.94705%205.97795%207.94485%205.98406%207.94265%205.99017L6.17057%209.36151C6.14408%209.41244%206.13085%209.46947%206.13305%209.5265V9.52752L6.17277%2010.6143C6.17718%2010.7202%206.22022%2010.819%206.29194%2010.8964L6.18712%2011.0919C6.14078%2011.1775%206.1794%2011.2814%206.27207%2011.3242C6.29856%2011.3364%206.32724%2011.3425%206.35483%2011.3425C6.42435%2011.3425%206.49056%2011.3069%206.52366%2011.2458L6.62516%2011.0553C6.64061%2011.0563%206.65495%2011.0573%206.6704%2011.0573C6.77412%2011.0573%206.87673%2011.0278%206.9628%2010.9687L7.91392%2010.325C7.93379%2010.3118%207.95254%2010.2955%207.96909%2010.2792C7.97241%2010.2761%207.97461%2010.2731%207.97793%2010.27C7.9989%2010.2476%208.01655%2010.2222%208.0309%2010.1957L10.1483%206.16942L10.2951%206.23461L9.35169%208.02823C9.30645%208.11379%209.34507%208.21768%209.43886%208.25943C9.46535%208.27165%209.49293%208.27674%209.52052%208.27674C9.59004%208.27674%209.65735%208.24109%209.68935%208.17896L10.7023%206.25293C10.7078%206.24581%2010.7133%206.23766%2010.7177%206.2295C10.7222%206.22134%2010.7244%206.21422%2010.7277%206.20606L10.9804%205.72533C11.0255%205.64082%2010.9858%205.53694%2010.8931%205.49519ZM6.73994%2010.6907C6.70574%2010.7131%206.6627%2010.7182%206.62408%2010.7049C6.61857%2010.7019%206.61305%2010.6988%206.60643%2010.6958C6.60312%2010.6948%206.60092%2010.6937%206.5976%2010.6927C6.5656%2010.6723%206.54575%2010.6398%206.54463%2010.6041L6.51814%209.89623C6.76641%2010.0745%207.05219%2010.2028%207.35673%2010.2741L6.73994%2010.6907Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3cpath%20d='M5.59896%2011.03C5.55151%2011.029%205.49634%2011.03%205.43897%2011.03C5.13885%2011.0331%204.57941%2011.0382%204.40067%2010.8538C4.36976%2010.8222%204.33005%2010.7652%204.3444%2010.647C4.38634%2010.314%204.58935%209.96362%204.76811%209.65499L4.79789%209.60305C4.85638%209.50221%204.91707%209.40036%204.97664%209.30056C5.14766%209.01537%205.32421%208.72%205.46433%208.40935C5.56806%208.18018%205.62542%207.96426%205.63536%207.7697C5.64859%207.50897%205.57799%207.28183%205.42571%207.09441C5.24365%206.86932%204.97774%206.70431%204.61361%206.58821C4.31128%206.49145%203.97806%206.44154%203.68455%206.39672C3.55215%206.37635%203.42635%206.35801%203.3105%206.33561C3.20899%206.31626%203.10969%206.37737%203.08982%206.47108C3.06885%206.56478%203.13505%206.65645%203.23658%206.67479C3.36015%206.69822%203.48926%206.71756%203.62497%206.73793C4.18219%206.82248%204.81444%206.91719%205.1256%207.30118C5.30986%207.52832%205.30766%207.85628%205.11788%208.2759C4.98547%208.56925%204.81444%208.85545%204.64783%209.13248C4.58825%209.23231%204.52646%209.33619%204.46687%209.43905L4.43709%209.48998C4.2418%209.82609%204.02111%2010.207%203.97146%2010.6053C3.9472%2010.7957%203.99795%2010.9567%204.12152%2011.084C4.38082%2011.3498%204.8939%2011.3763%205.29223%2011.3763C5.34408%2011.3763%205.39485%2011.3763%205.44229%2011.3753C5.49855%2011.3753%205.55043%2011.3743%205.59456%2011.3753C5.59566%2011.3753%205.59566%2011.3753%205.59676%2011.3753C5.69939%2011.3753%205.78324%2011.2989%205.78434%2011.2041C5.78544%2011.1105%205.70266%2011.031%205.59896%2011.03Z'%20fill='white'%20style='fill:white;fill-opacity:1;'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_10486_8655'%3e%3crect%20width='7.91304'%20height='7.30435'%20fill='white'%20style='fill:white;fill-opacity:1;'%20transform='translate(3.08594%204.12891)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Review and sign your document